Mumbai: Despite global economic headwinds, including lay-offs by several large and small corporates, the bull run in the Indian housing market continued in the first quarter of the year. Quarterly housing sales are at an all-time high in the last decade, with approximately 1,13,770 units sold in Q1 2023 across the top seven cities, reveals research. This is a 14% yearly rise against approx. 99,550 units sold back in Q1 2022.

The two leading western markets Mumbai Metropolitan Region (MMR) and Pune accounted for over 48% of the total sales in the top seven cities, with Pune witnessing an over 42% yearly jump, revealed a recent study conducted by Anarock group.

Also Read: 4 lakh homes made in 2022 across top 7 cities, highest in a year

New launches across the top seven cities also breached the one lakh mark and witnessed 23% yearly rise – from 89,140 units in Q1 2022 to over 1,09,570 units in Q1 2023. Interestingly, MMR and Pune again saw the maximum new supply, accounting for 52% of the total new launches across the top cities. Individually, the two cities saw 58% and 34% yearly increases in their new supply, respectively.

Despite spiralling new launches in this and the previous quarter, the available inventory in the top seven cities remained almost similar at about 6.27 lakh units by Q1 2023-end. On a Q-O-Q basis, unsold stock saw a 1% dip across the top 7 cities. Among the top cities, NCR saw highest decline in its unsold stock in Q1 2023 by 22%.

Anuj Puri, chairman – Anarock Group, says, “The residential market’s winning streak continued in the first quarter of 2023 with housing sales in top cities breaching the previous high of Q1 2022. The quarter has recorded the highest ever sales in the last decade amid significant rise in demand for high-ticket priced homes (more than ₹1.5 Cr).”

Also Read: Property price rises by 11-14% in Pune, Delhi & NCR on YoY basis

“However, emerging headwinds could pose a challenge in the short-term,” says Puri. “Persistent inflation concerns along with another possible rate hike by the RBI in the near future could dent the housing market’s growth trajectory in the upcoming two quarters. Once the dust of the ongoing economic disruptions settles, it is likely to regain again, backed by rise in home ownership sentiment,” added Puri.

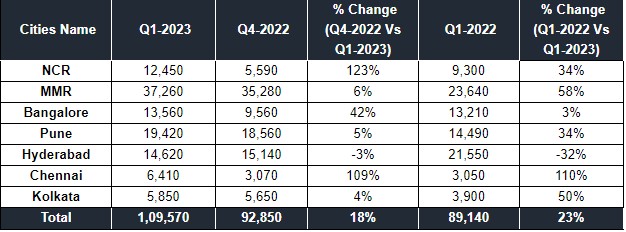

New launch overview

The top seven cities recorded new launches of around 1,09,570 units in Q1 2023 against 89,140 units in Q1 2022, increasing by 23% over the previous year’s corresponding period. The key cities contributing to new launches in Q1 2023 included MMR, Hyderabad, Pune, and Bengaluru, together accounting for 77% supply addition.

MMR saw nearly 37,260 units launched in Q1 2023–a significant increase of nearly 58% over Q1 2022. More than 62% new supply was added in the sub-₹80 lakh budget segment. Pune added new supply of about 19,420 units in Q1 2023 compared to 14,490 units in Q1 2022–an increase of 34%.

Hyderabad added nearly 14,620 units in Q1 2023, a yearly decline of 32% over the corresponding period last year. Over 52% new supply was added in the high-ticket price segment priced more than ₹1.5 Cr.

Bangalore added about 13,560 units in Q1 2023, yearly increase of just 3%. Nearly 74% new supply was added in the mid-range and premium segments, i.e., the ₹40 Lakh – ₹1.5 Cr price bracket.

NCR saw an increase of 34% in new launches against Q1 2022 with approx. 12,450 units launched in Q1 2023.

Chennai added about 6,410 units in Q1 2023, a yearly increase of whopping 110% over Q1 2022. It was the only city to see three-digit growth in new supply.

Kolkata added about 5,850 units in Q1 2023, an increase of 50% over Q1 2022. About 70% new supply was added in the mid segment priced between ₹40 lakh–₹80 Lakh.

City wise supply (in units) and Q-o-Q % change

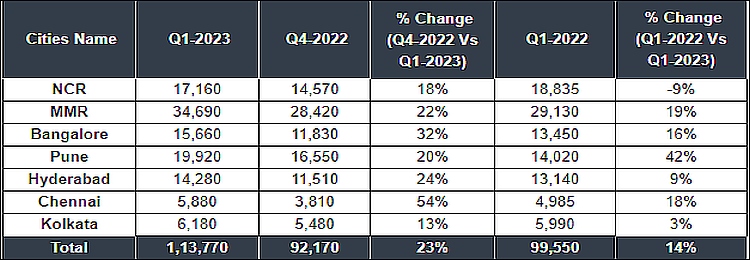

Overall Sales Overview

About 1,13,770 units were sold in Q1 2023–an increase of 14% over Q1 2022. NCR, MMR, Bengaluru, Pune, and Hyderabad together accounted for 89% sales in the quarter.

Pune saw 19,920 units sold in Q1 2023, increasing by 42% over Q1 2022. NCR is the only city to see a decline (of 9%) in housing sales among all cities – from 18,835 units in Q1 2022 to nearly 17,160 units in Q1 2023.

Housing sales in Kolkata increased by 3% over Q1 2022, with nearly 6,180 units sold in Q1 2023.

MMR and Bangalore saw housing sales increase by 19% and 16% respectively in Q1 2023 against Q1 2022, with about 34,690 and 15,660 units sold, respectively. Chennai saw around 5,880 units sold-an increase of 18% over Q1 2022. Hyderabad recorded sales of 14,280 units in Q1 2023, a spike of 9% over Q1 2022.

City wise absorption (in units) and Q-o-Q percentage change

Price Movement

Average residential property prices across the top seven cities increased in the range of 6-9% in Q1 2023, when compared to Q1 2022, mainly due to increase in the prices of construction raw materials and overall rise in demand. MMR and Bangalore recorded the highest 9% annual jump.

Available Inventory

Despite massive new supply being added to the top cities in Q1 2023, it was observed that available inventory stay more or less static in Q1 2023 as compared to Q1 2022. The total available inventory in the top cities as of Q1 2023-end stands at around 6.27 lakh units. NCR witnessed the highest reduction in available inventory in Q1 2023 when compared to Q1 2022-by 22%.

- Of total 1.14 lakh units sold across top 7 cities in Q1 2023, approx. 24% were in the high-ticket segment priced more than ₹1.5 Cr

- Quarterly sales numbers at all-time high; annually, top cities register over 14% Y-o-Y rise in sales against 99,550 units sold in Q1 2022

- MMR & Pune account for 48% of total sales; Pune records 42% yearly jump

- New launches also breach the one lakh mark, rise 23% Y-o-Y – from 89,140 units in Q1 2022 to approx. 1.10 lakh units in Q1 2023

- MMR & Pune account for 52% of total launches in top cities; Hyderabad only city to see new supply dip in quarter (by 32% yearly)

- Mid-segment homes priced ₹40-₹80 lakh continue to dominate new supply with 36% share, followed by premium (₹80 lakh–₹1.5 Cr) & affordable segments (less than ₹40 lakh) with 24% & 18% shares respectively

- Despite surge in new supply, available inventory in top seven cities remained the same at 6.27 lakh units; NCR witnessed highest yearly inventory decline of 22%

- Average property prices in top 7 cities see 8% yearly rise–Bangalore & MMR record highest 9% increase each

")